Although major exposures of accounting mismatches and errors are relatively rare in Nepal, a recent event in India have highlighted the potential risks. The event involved a currency valuation error, which led to a mismatch in derivative hedging strategies, resulting in substantial financial losses for both a bank and its investors. This incident serves as a stark reminder of how even minor miscalculations in financial management can have far-reaching consequences in today’s complex economic environment.

About the Bank

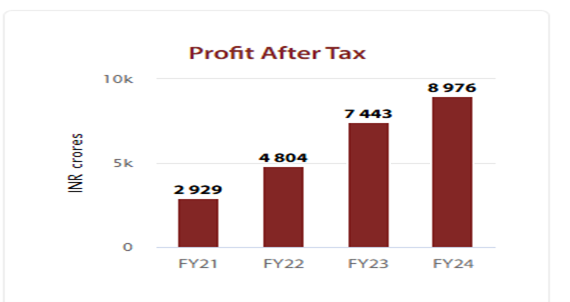

IndusInd Bank was founded in 1994 and was one of the nine banks that received a banking license that year. The bank was established by S. P. Hinduja, along with several NRI and other investors. The name “IndusInd” is inspired by the ancient Indus Valley Civilization, which connects the bank to India’s rich heritage of past. The bank commenced its operations on April 17, 1994, with a formal inauguration by Dr. Manmohan Singh, who was the Union Finance Minister at the time. In 1997, IndusInd Bank went public by launching its Initial Public Offering (IPO), a significant step in its growth within the Indian financial sector. The bank has achieved a solid growth over past years as evidenced by the profit growth.

In the recent days IndusInd Bank is grappling with a significant issue stemming from an “accounting discrepancy” in its forex hedging strategy, which has resulted in a sharp 27% drop in its stock price on March 11, 2025. While the problem does not pose an immediate threat to depositors, it has raised concerns about the bank’s financial management and risk oversight. Forex hedging is crucial for mitigating currency risks, and such discrepancies can erode investor confidence, especially in the unpredictable banking industry. As the bank works to resolve the matter, it underscores the importance of clear communication and solid financial controls to preserve trust with investors and customers. This situation could also prompt closer scrutiny of other banks’ risk management practices in the future. The recent disclosure of bank include the following statement:

“During an internal review of processes relating to other assets and other liability accounts of the derivatives portfolio, the Bank has noted some discrepancies. Since then, the Bank’s internal review has estimated an adverse impact of 2.35% on the Bank’s net worth as of December ’24. The difference has been accumulated over a period of time. The Bank’s profitability and capital adequacy remains healthy to absorb this one-time impact. Just to reiterate the issue was identified by the Bank. We also appointed an external advisor to review the processes and ascertain the root cause” (extract of Analyst Conference Call of Bank on March 10, 2025)

Risky Business: The NRI Deposit Strategy and Its Impact on IndusInd Bank

IndusInd Bank’s aggressive strategy to attract NRI deposits, offering appealing interest rates to tap into foreign currency inflows, appeared to be a shrewd move. By Q3 FY25, the bank had accumulated ₹58,600 crore in NRI deposits, accounting for 14.3% of its total deposits, which stood at ₹4.09 lakh crore. NRI deposits are typically seen as a reliable source of long-term liquidity, offering stability to a bank’s balance sheet. However, the bank’s reliance on complex forex hedging mechanisms to manage the associated currency risk backfired when an accounting mismatch resulted in an unexpected ₹1,580 crore loss in Q4 FY24, roughly 2.3% of its total net worth. This incident highlights the risks involved in sophisticated financial strategies and the importance of sound risk management practices to prevent such discrepancies.

Unraveling the Loss: A Detailed Analysis of How IndusInd Bank’s Forex Hedging Strategy Misfired”

IndusInd Bank’s strategy to manage foreign exchange risk on NRI deposits involved complex transactions through its Asset-Liability Management (ALM) Desk and Trading Desk. When an NRI deposits $1 million, the bank converts it into rupees, providing liquidity that can be lent or invested. However, when the deposit matures, the bank must return the amount in dollars, and any unfavorable exchange rate changes can result in significant losses.

To manage this risk, the ALM Desk shifts the liability to the Trading Desk through internal derivatives, which are then externally hedged with global banks using currency swaps to lock in exchange rates. While the internal and external hedges are meant to offset each other, a mismatch arose due to the use of different valuation methods. The external hedge was marked to market daily, while the internal hedge followed swap cost accounting. This led to a significant discrepancy, especially when the bank repaid foreign borrowings earlier than planned. The error in accounting, which mistakenly recorded the loss as “intangible assets,” resulted in a ₹1,580 crore loss, around 2.35% of the bank’s net worth. This exposed flaws in the bank’s risk management and accounting practices, causing investor concerns, although the final amount may vary after statutory audit adjustments and central bank oversight.

Leadership concerns?

While this decision may appear to reflect transparency, there are signs that the Reserve Bank of India (RBI) may have influenced the bank’s timing. The bank’s disclosure came just three days after the RBI extended CEO’s tenure for only one year, rather than the three years he had requested. This timing raises questions about the role of the regulator in pushing the bank to be more transparent.

Additionally, new RBI regulations on the classification, valuation, and operations of investment portfolios—set to take effect in April 2024—required banks to review their derivative positions. While most banks had disclosed the impact of these changes by June 2024, IndusInd Bank chose to delay its own disclosure until March 2025. This delay, combined with the timing of the CEO’s tenure decision, suggests that external pressures, including regulatory nudging from the RBI, may have played a significant role in the bank’s eventual disclosure of the forex-related losses. This sequence of events highlights the delicate balance between corporate decision-making and regulatory oversight in the Indian banking sector.

Tremors Reverberates Beyond Walls

The Reserve Bank of India (RBI) has begun a review of derivative books of both private and state-owned banks after IndusInd Bank reported discrepancies in accounting related to forex derivatives (https://www.moneycontrol.com/news/business/rbi-starts-industry-wide-review-of-derivative-positions-after-indusind-bank-fiasco-12962797.html)

Private lender IndusInd Bank’s stock has been put under short term Additional Surveillance Measure (ASM) – Stage 1 by the NSE. The decision was taken on March 13 following a nearly 30% fall after accounting discrepancies were reported by the bank. (https://economictimes.indiatimes.com/markets/stocks/news/nse-puts-indusind-bank-under-additional-surveillance-after-derivatives-discrepancies/articleshow/118983043.cms?from=mdr)

The bank’s share price have tanked in the NSE and BSE significantly

Summing up

IndusInd Bank’s forex hedging loss, although not fraudulent, has exposed significant accounting lapses that have eroded investor confidence. While the bank’s decision to disclose the issue promptly is a positive step, the mismatch in its risk management practices has raised concerns about its financial controls and oversight. Moving forward, the bank must prioritize greater transparency in its operations and implement stronger risk management frameworks to reassure investors. By taking decisive action to address these weaknesses and providing clear, consistent communication, IndusInd Bank can begin to rebuild trust and stabilize its position in the market. Reaffirming its commitment to robust financial practices will be crucial in restoring confidence among both investors and clients.